When you’re standing in a crowded subway car during rush hour, your wallet in your front pocket, squeezed by dozens of strangers. Somewhere in the crowd, someone might be holding a device—no bigger than a smartphone—capable of reading your credit card information from a distance.

Sound like science fiction? It’s not. This is known as RFID skimming. While the actual risk is lower than some alarmists claim, the technology is very real. The question isn’t whether you should protect yourself—it’s how.

You’ve likely seen two solutions: RFID-blocking cards (thin inserts for your wallet) and RFID-blocking wallets (wallets lined with protective material). Both promise protection, but which one actually works?

The Real Talk About RFID Threats

Before we compare solutions, let’s get honest about the threat level.

Yes, RFID skimming is technically possible. A thief with the right equipment can scan your contactless payment card from a few centimeters away—up to 10cm in some cases. In 20 minutes, a skilled criminal could theoretically gather details from 50 cards just by walking through a busy shopping center.

But here’s the reality check: Most modern credit and debit cards use EMV encryption and dynamic transaction codes. Even if someone scans your card, the stolen data is typically useless for making purchases. The three-digit CVV code on the back isn’t transmitted via RFID.

That said, older access badges, hotel key cards, and some passports remain more vulnerable. And while your bank will likely reimburse fraudulent charges, there’s a catch: you have 60 days to report it. Miss that window, and your financial institution isn’t obligated to help. Plus, during the investigation, those funds may be frozen—a serious problem when six in ten Americans don’t have $500 saved for emergencies.

So the threat isn’t Hollywood-level dramatic, but it’s real enough to warrant smart, affordable protection.

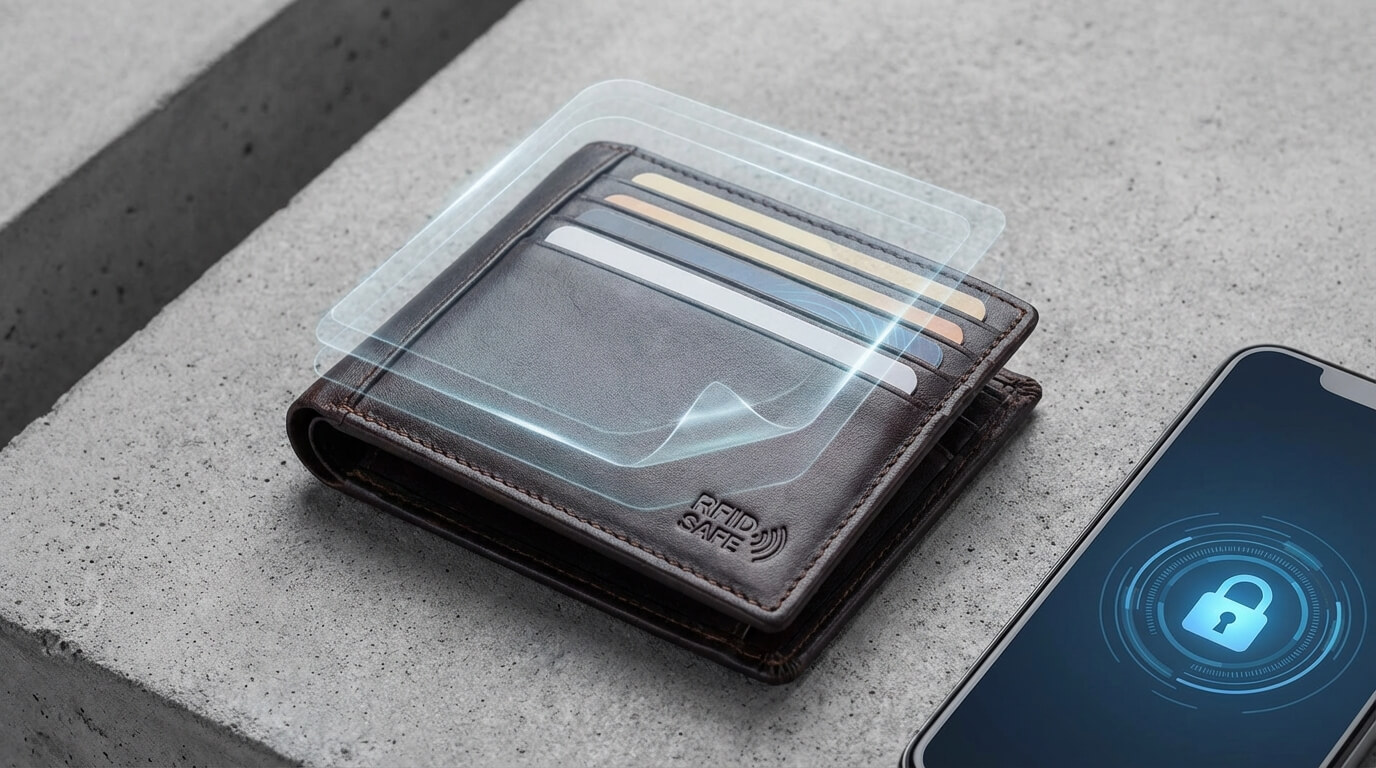

How RFID Blocking Actually Works

Both blocker cards and blocking wallets use electromagnetic shielding—think of it as a Faraday cage for your wallet. They absorb or deflect radio waves at specific frequencies, preventing your card’s chip from communicating with unauthorized scanners.

The critical detail: Most contactless payment cards operate at 13.56 MHz (high frequency). Older access cards use 125 kHz (low frequency). Quality blocking products must be tuned to the right frequency, or they won’t work.

Here’s where the two solutions diverge:

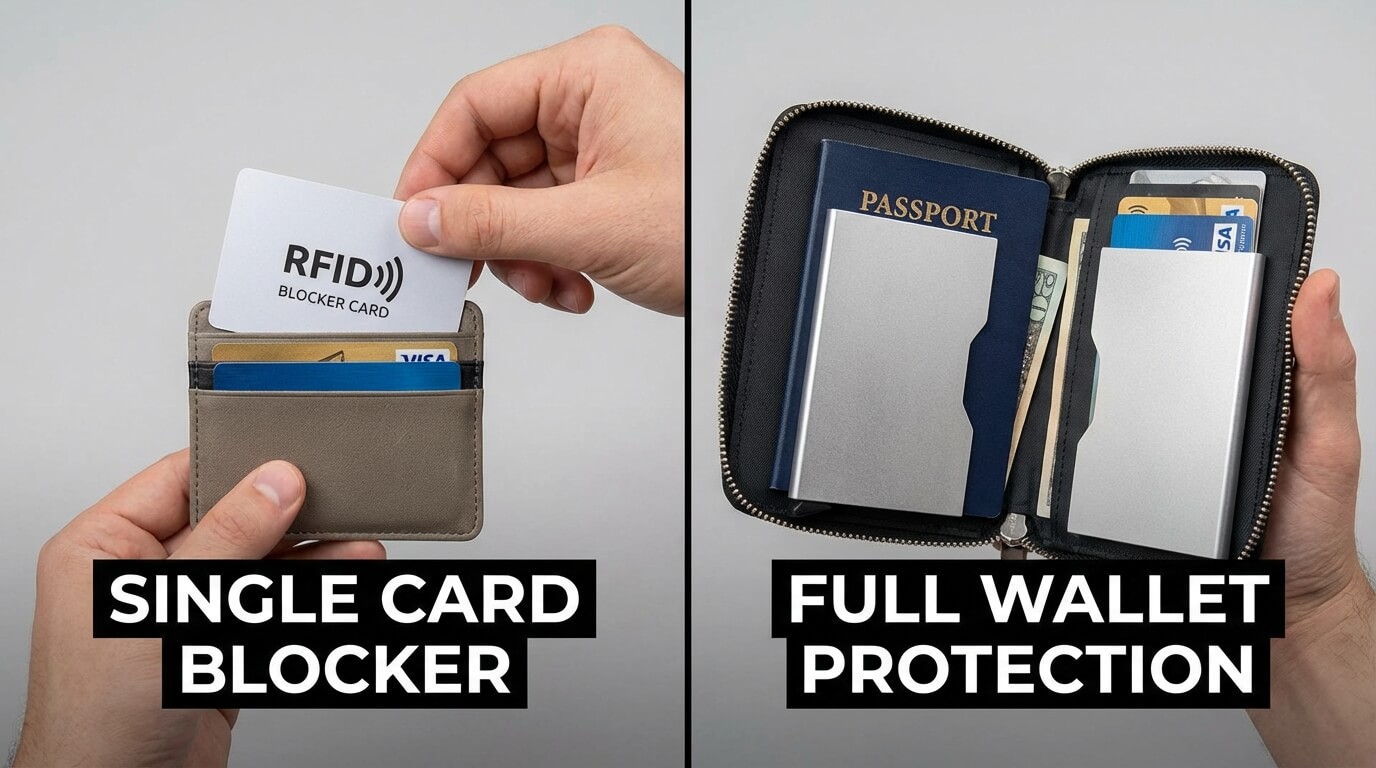

RFID Blocker Cards: Active Jamming

A blocker card is a single card—same size as a credit card—that you slide into your wallet next to your RFID-enabled cards. High-quality versions (like WXR’s solutions) use active jamming technology. Instead of just reflecting signals, they actively scramble scanning attempts, creating interference within about 2cm on either side of the card.

How to use it: Slip it into any wallet slot, front or back, upside down or right-side up—orientation doesn’t matter. For maximum protection, sandwich your payment cards between two blocker cards, or place one in the middle of your card stack.

RFID-Blocking Wallets: Passive Shielding

These wallets have conductive material (often metallic fabric or carbon fiber) built into the lining. Every compartment is shielded, protecting all cards inside simultaneously.

The catch: You’re locked into that specific wallet design. If you want to switch styles or brands, you start over.

The Head-to-Head Comparison

Let me break down the practical differences based on real-world testing and user feedback:

| FACTOR | RFID BLOCKER CARD | RFID-BLOCKING WALLET |

|---|---|---|

| Protection Method | Active jamming—scrambles signals | Passive shielding—blocks signals |

| Flexibility | Works in any wallet you already own | Limited to that specific wallet design |

| Cost | $15–$30 per card | $40–$120+ for entire wallet |

| Convenience | Stays in wallet; no extra steps | Must remove cards from shielding to use |

| Bulk | 0.9mm thin—same as credit card | Often bulkier than standard wallets |

| Coverage | Protects cards within 2cm radius | Protects all compartments |

| Replacement | Easy—just swap the card | Must buy entirely new wallet |

| Testing | Can verify with NFC Tools app | Harder to test individual card protection |

Why Operations Managers Choose Blocker Cards

In my experience working with corporate clients—think warehouse managers, retail operations teams, and system integrators—the blocker card wins on three fronts:

1. Scalability

You’re outfitting 50 employees with access badges. Buying 50 RFID-blocking wallets? That’s $2,000–$6,000. Buying 50 blocker cards? Under $1,500. Plus, employees can use their preferred wallets.

2. Compatibility

A single high-quality blocker card protects both RFID and NFC signals. It works with payment cards, employee IDs, hotel keys, and transit passes—all from one slim card. A blocking wallet only protects what’s inside its specific compartments.

3. No Behavior Change

With a blocker card, your team doesn’t change habits. The card stays in the wallet, always on guard. With a blocking wallet, users must remember to remove cards from shielded sleeves before tapping at payment terminals—an extra step that gets forgotten during busy shifts.

Why Brand Managers Love the Blocker Card Story

If you’re in marketing or product development, here’s the narrative gold: The blocker card is a symbol of smart, minimalist protection.

It’s not bulky. It’s not paranoid. It’s the kind of everyday insurance that says, “I’m prepared, but I’m not living in fear.” That’s a message that resonates with consumers who value both security and style.

Real-world example: A retail brand we worked with gave blocker cards to loyalty program members as a thank-you gift. The response? Members posted photos on social media, praising the brand for “actually caring about our safety.” The cards became conversation starters—free word-of-mouth marketing.

Compare that to handing out branded wallets. Sure, it’s a nice gift, but it forces recipients to abandon their current wallet. The blocker card? It enhances what they already love.

The Wallet’s One Big Advantage

Let’s be fair: RFID-blocking wallets offer comprehensive, set-it-and-forget-it protection. If you carry multiple RFID-enabled items—payment cards, passports, employee badges, transit cards—a shielded wallet protects everything simultaneously without requiring strategic card placement.

Best use case: International travelers who carry passports with RFID chips. A blocking wallet ensures the passport is always shielded, even if you forget about it.

But here’s the reality: Most people don’t carry passports daily. For everyday protection of payment cards and IDs, a blocker card delivers the same security with far more flexibility.

What About Those Cheap Alternatives?

You’ve seen them on Amazon: RFID-blocking sleeves for $5, or no-name blocker cards for $8.

Here’s what independent testing shows: Low-quality blockers may stop weak scanners but fail against readers with stronger antennas or amplified power. ZDNET tested a budget blocker against a Flipper Zero device (a popular hacking tool) and found inconsistent protection.

Why quality matters:

- Material integrity: Cheap cards use thin shielding that degrades quickly.

- Frequency tuning: Budget products often aren’t properly calibrated to 13.56 MHz.

- No battery required: Quality active jammers don’t need batteries—they’re always on. Cheap versions may use passive blocking that’s less effective.

Think of it this way: You wouldn’t buy a $5 bike lock to protect a $2,000 bicycle. Why trust a $5 blocker to protect your financial identity?

How to Test Your Blocker Card (In 60 Seconds)

Don’t take anyone’s word for it—test it yourself:

Method 1: The NFC Tools App

- Download “NFC Tools” from Google Play or the App Store (it’s free).

- Scan any RFID-enabled credit or debit card with your phone. You’ll see data appear.

- Place your blocker card next to the payment card.

- Try scanning again. If the blocker works, the data will be scrambled or unreadable.

Method 2: The Self-Checkout Test

- Go to a grocery store with contactless payment terminals.

- Hold your blocker card over your payment card.

- Wave both cards together over the reader.

- If the blocker works, the terminal won’t detect your card.

This kind of transparency builds trust. You’re not asking customers to “just believe”—you’re giving them proof.

The Bottom Line: Which Should You Choose?

Choose an RFID blocker card if:

- You want flexibility to use any wallet

- You’re protecting 1–5 cards (payment cards, work badge)

- You value slim, minimalist design

- You want active jamming technology

- You’re outfitting a team or organization

Choose an RFID-blocking wallet if:

- You carry multiple RFID items daily (passport, transit cards, etc.)

- You prefer all-in-one solutions

- You’re buying a new wallet anyway

- You don’t mind the extra bulk

Pro tip from the field: Many security-conscious professionals use both. They keep a blocker card in a standard wallet for daily use, and switch to a blocking wallet when traveling internationally. Layered protection, tailored to the situation.

A Final Word on Smart Security

RFID blocking isn’t about paranoia—it’s about proportional response. The threat is real but manageable. You don’t need to live in fear, but you also shouldn’t ignore simple, affordable safeguards.

A quality blocker card offers active protection, fits any lifestyle, and costs less than a nice dinner. It’s the kind of everyday insurance that just makes sense—like locking your car or using a password manager.

And if you’re a business leader or brand manager? It’s a chance to show your team or customers that you’ve thought about their security in a practical, non-intrusive way.

Want to explore RFID solutions that actually fit your operations? Whether you’re securing employee badges, protecting customer data, or building a brand story around smart security, WXR‘s team has the experience and certifications to guide you. Let’s talk about what protection looks like in your world—not in a marketing brochure.